Understanding Blockchain: The Revolutionary Technology Powering Web3

In a world that's increasingly leaning towards digitalization, the introduction of blockchain technology has undoubtedly become a game-changer. But what exactly is blockchain? Simply put, a blockchain is a continuously growing chain of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic principles, creating a public, decentralized ledger of all transactions that's transparent and immutable.

This technology has become the backbone of the Web3 revolution – the new phase of the internet that aims to create a decentralized and secure digital space. Blockchain serves as the fundamental infrastructure of Web3, providing the base upon which other key Web3 elements such as cryptocurrencies, smart contracts, and decentralized applications (dApps) are built.

This technology's disruptive potential goes beyond just finance or technology; it has the ability to revolutionize many sectors, including healthcare, supply chain, and more. It's not just about decentralizing money anymore—it's about decentralizing the whole web.

In this article, we'll explore the concept of blockchain in detail. We'll delve into its workings, features, applications, and how it powers the new decentralized age of the internet – Web3. Whether you're a blockchain novice or someone looking to brush up their knowledge, this comprehensive guide will give you a deep understanding of this revolutionary technology.

Evolution of Blockchain Technology

The story of blockchain begins with the emergence of Bitcoin. In 2008, an individual or group known under the pseudonym Satoshi Nakamoto released a white paper introducing Bitcoin and its underlying blockchain technology to the world. This was in response to the 2008 financial crisis and a growing desire for a financial system independent of central authorities.

Bitcoin's blockchain was designed as a public ledger for all transactions happening in the Bitcoin network. This was a groundbreaking idea – a decentralized, peer-to-peer (P2P) system that could verify transactions without the need for a central authority. This not only introduced the world to a new form of currency (Bitcoin), but also to an entirely new way of recording data—blockchain.

The core principles established by Bitcoin's blockchain – decentralization, transparency, and immutability – have remained constant. However, the technology has significantly evolved over time. Ethereum, launched in 2015, introduced the concept of programmable contracts or smart contracts, expanding the use cases of blockchain beyond just transferring digital assets.

This spurred the development of many other blockchain platforms, each with its own unique features and focuses. For instance, Cardano aims to solve issues of security, scalability, and interoperability in blockchain. Solana, on the other hand, offers high-speed and low-cost transactions.

Besides the development of new platforms, the technology has also seen evolution in terms of its consensus mechanisms. While Bitcoin uses proof-of-work (PoW) for achieving consensus, newer blockchains like Ethereum are using proof-of-stake (PoS), which is considered more energy-efficient.

From the creation of Bitcoin to the rise of various blockchain platforms, blockchain technology has come a long way. Its applications have diversified, its efficiency has improved, and its influence has broadened. As we dive deeper into the era of Web3, the evolution of this technology continues, providing more opportunities and potential for a decentralized future.

Blockchain Explained: How It Works

Understanding the inner workings of blockchain technology can seem daunting at first. However, breaking it down into its essential components can make it much more digestible.

Blocks and Their Contents

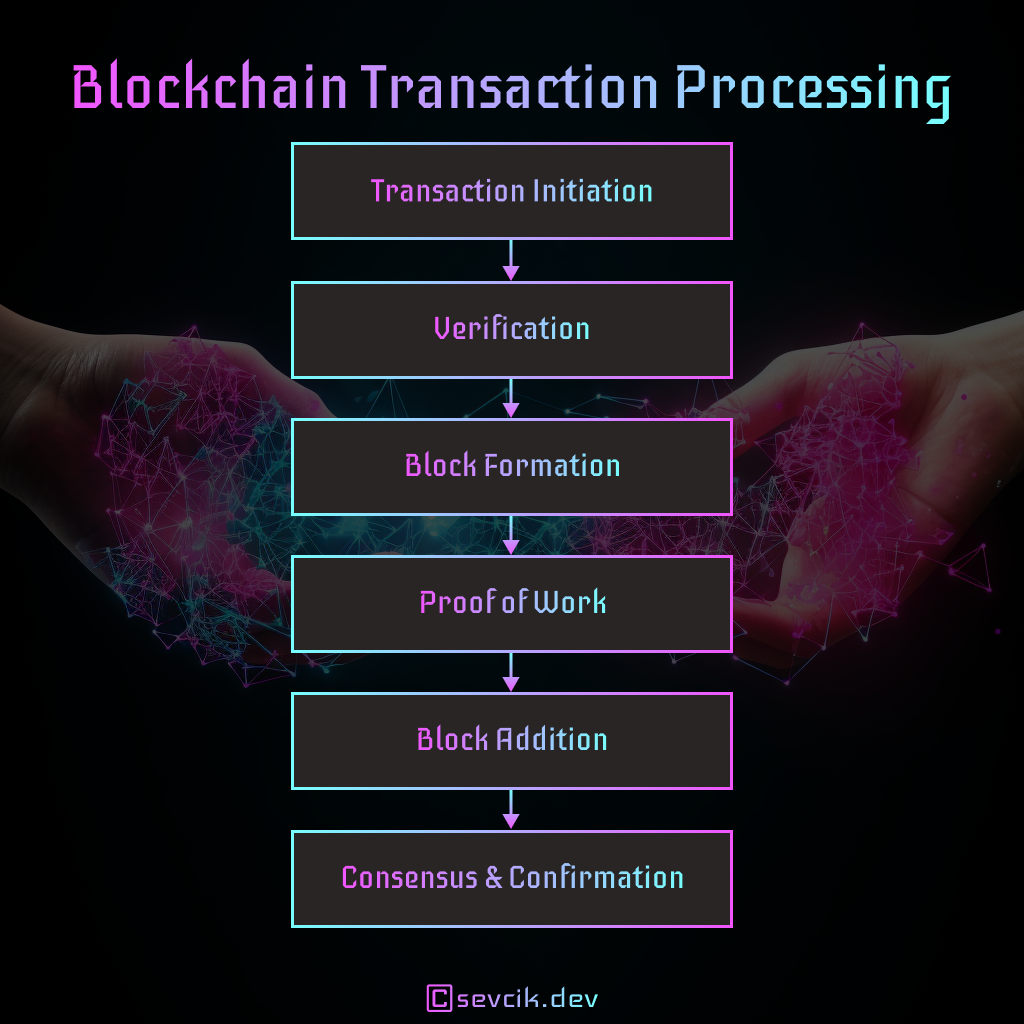

A blockchain, as the name suggests, is a chain of blocks. Each block contains a list of transactions. For instance, in the case of Bitcoin, a transaction could represent the transfer of bitcoins from one person to another. Each transaction within a block is verified by participants in the network, known as nodes.

Aside from transactions, a block also contains a unique hash. A hash is a cryptographic string of characters that is generated by applying a hash function to the block's content. It's like a digital fingerprint—unique to each block. Changing any data within the block will change its hash, making tampering with blockchain data easily detectable.

A block also contains the hash of the previous block in the chain, creating a link between them. This linkage is what forms a blockchain.

Chain Formation and Cryptographic Principles

The blockchain's security lies in its cryptographic principles. As mentioned, each block contains the hash of the previous block. This means if someone tries to alter the data in a block, it will not only change the hash of that block but also break the link with the next block. To restore the link, they would have to change the data in every subsequent block, which is practically impossible due to the time and computational power needed.

This makes the blockchain extremely secure and renders the data recorded on it immutable, or unchangeable.

Decentralization and Consensus Mechanisms

Unlike traditional databases, which are centrally controlled, a blockchain is decentralized. The data isn't stored in a single location but distributed across a network of computers, or nodes. Each node has a copy of the entire blockchain, and all nodes work together to maintain and update the blockchain.

A crucial aspect of maintaining a blockchain is achieving consensus among nodes on the validity of transactions. This is where consensus mechanisms come into play.

The two most common consensus mechanisms are Proof of Work (PoW) and Proof of Stake (PoS).

PoW, used by Bitcoin, involves solving complex mathematical problems, or "mining," to add new blocks to the chain. It's a competitive process where the first miner to solve the problem gets to add the block and is rewarded with bitcoins.

PoS, used by blockchains like Ethereum, selects validators to add new blocks based on their stake, or amount of cryptocurrency, held. This mechanism is considered to be more energy-efficient than PoW.

Types of Blockchain

Blockchain technology has a wide range of applications, and not all of them require the same level of transparency or decentralization. To cater to different needs, we have different types of blockchains: public, private, and consortium blockchains.

Public Blockchains

Public blockchains are open to anyone who wants to participate. They are decentralized and transparent, meaning anyone can join the network, validate transactions, and create new blocks. Bitcoin and Ethereum are classic examples of public blockchains.

These blockchains provide a high level of security, and since they are open source, they foster innovation. However, they can be slower and more resource-intensive due to their consensus mechanisms like PoW or PoS.

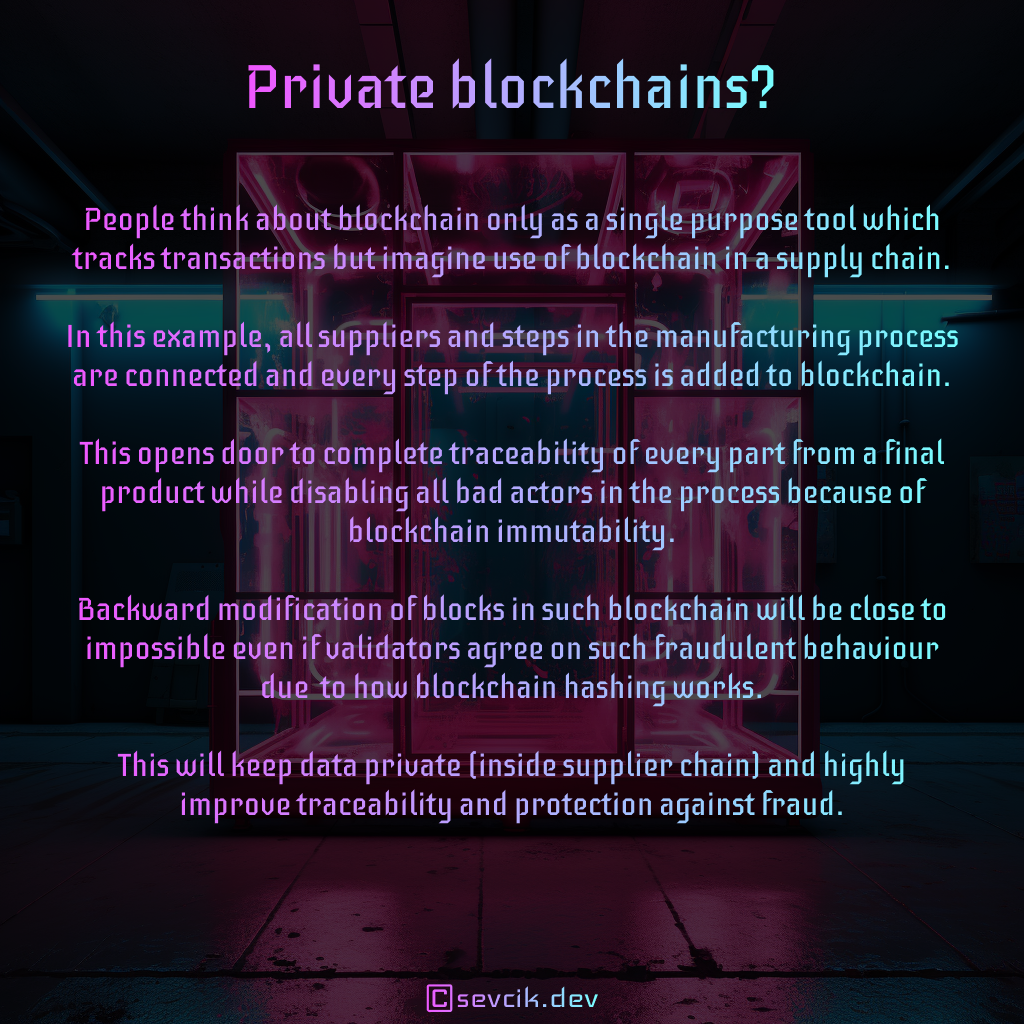

Private Blockchains

Unlike public blockchains, private blockchains are permissioned. They are only accessible to a selected group of participants who have been invited to join. Private blockchains are typically used by businesses and organizations for internal purposes.

Private blockchains can process transactions faster and with more efficiency as they don't require the intensive consensus mechanisms used in public blockchains. However, they are not as decentralized or transparent as public blockchains.

Consortium Blockchains

Consortium blockchains, also known as federated blockchains, are a middle ground between public and private blockchains. They are semi-decentralized and are controlled by a group of organizations rather than a single one.

The consortium, or group of organizations, determines who can join the network and participate in the consensus process. This type of blockchain is beneficial when multiple organizations need to collaborate and share data, but still require control over who can access the information.

Differences and Use Cases for Each Type

Each type of blockchain serves different needs and use cases:

- Public Blockchains are ideal for cryptocurrencies like Bitcoin and Ethereum, decentralized applications (dApps), and initiatives that require transparency, security, and public verification.

- Private Blockchains are used by businesses and organizations for internal processes like interdepartmental transfers or auditing. They are useful when a single organization wants to use blockchain's benefits but requires privacy and control over the network.

- Consortium Blockchains are used when multiple organizations need to collaborate but want to retain some level of privacy and control. Use cases can include supply chain management, banking, and healthcare record management.

In summary, the type of blockchain used depends on the specific requirements of transparency, decentralization, and control of the network.

Key Features of Blockchain

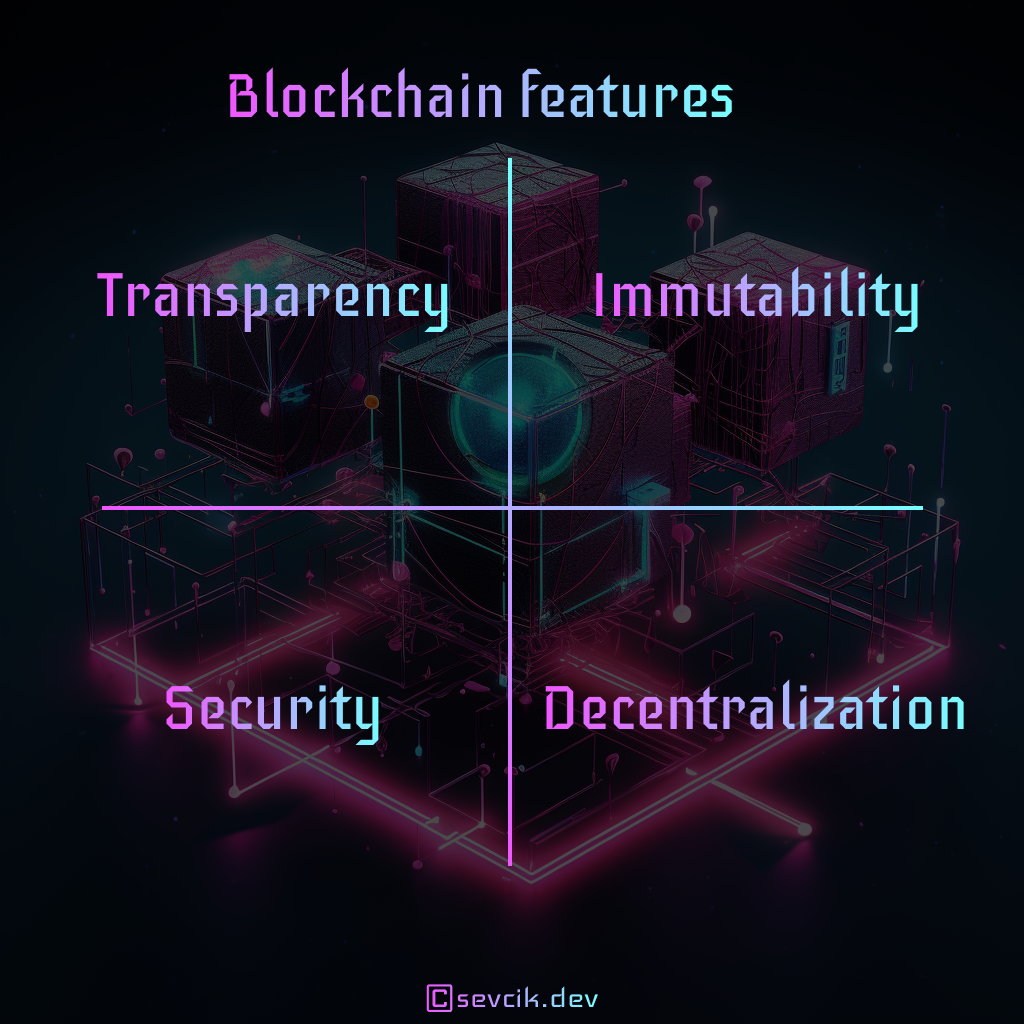

Blockchain technology has been hailed as revolutionary, mainly because of the unique features it brings to the table. These features combine to make blockchain a powerful tool for various applications across many sectors.

Transparency and Public Verification

One of the main features of blockchain is its transparency. In public blockchains, every transaction is recorded on the blockchain and is visible to all participants in the network. This makes it extremely difficult to manipulate the system without others noticing.

Additionally, the process of adding new transactions to the blockchain involves a public verification process. This means that multiple participants (nodes) in the network validate each transaction, ensuring its authenticity.

Immutability

Another crucial feature of blockchain is its immutability—once data is added to the blockchain, it can't be changed. This is ensured by the cryptographic hash functions we discussed earlier. If anyone tries to alter the data in a block, it changes the block's hash, making the tampering evident. This feature is essential in creating trust in the system, especially in scenarios where data integrity is vital, such as financial transactions or legal contracts.

Security and Decentralization

Blockchain technology is inherently secure, thanks to its decentralized nature. Instead of being stored in a central location, copies of the blockchain are distributed across a network of nodes. This decentralization makes the system highly resistant to attacks. Even if an attacker manages to take down one node, the others remain unaffected, keeping the blockchain intact and running.

Smart Contract Functionality

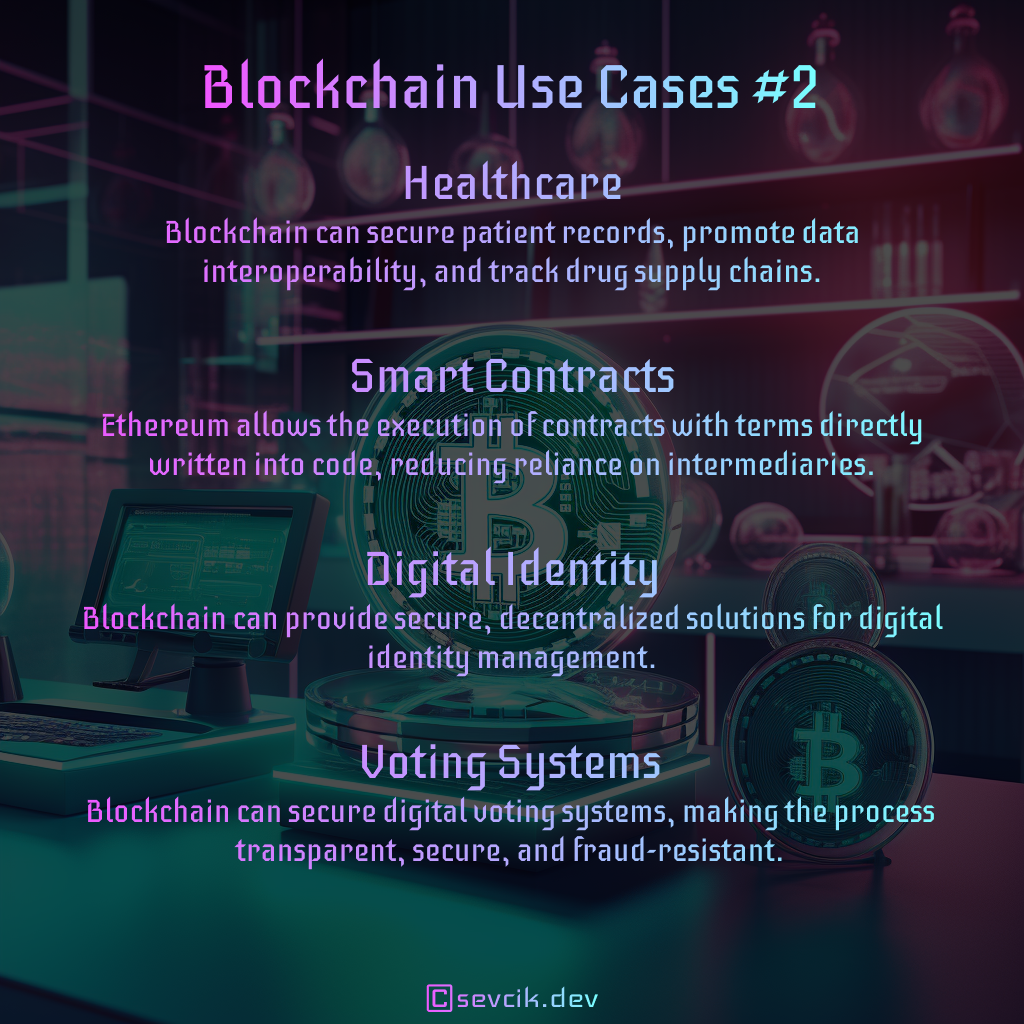

A particularly notable feature introduced with the Ethereum blockchain is the ability to create smart contracts. A smart contract is a self-executing contract with the terms of the agreement directly written into lines of code.

When predetermined conditions are met, the smart contract automatically performs the agreed actions, eliminating the need for a middleman. This opens up a whole new realm of possibilities for automatic, trustless interactions, forming the backbone of decentralized applications (dApps) and Decentralized Finance (DeFi) platforms.

In summary, the key features of blockchain—transparency, immutability, security, and smart contract functionality—are what make it a transformative technology. These features serve as the foundation for a new, decentralized era of the internet—Web3.

Real-world Applications of Blockchain

Blockchain's unique features have made it attractive for a variety of real-world applications, beyond just the realm of digital currencies. Here are some of the significant applications that have been transforming industries:

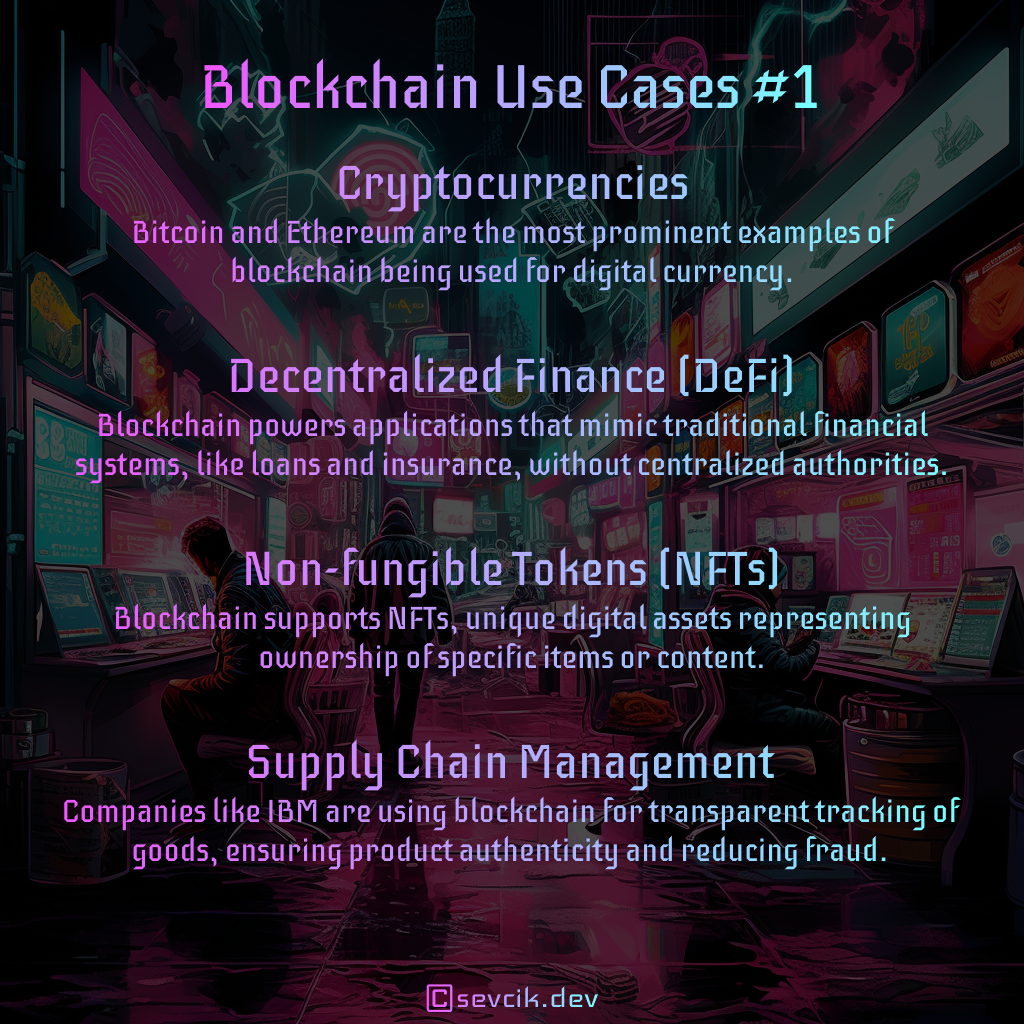

Cryptocurrencies

The most well-known application of blockchain is cryptocurrencies. Bitcoin, the first application of blockchain technology, introduced a decentralized, digital currency free from any central authority's control. Since then, many other cryptocurrencies like Ethereum, Litecoin, and Ripple have surfaced, each with its unique features and uses.

Decentralized Finance (DeFi)

Decentralized Finance, or DeFi, is another significant application of blockchain. DeFi uses blockchain's smart contract functionality to recreate and improve upon traditional financial systems, but in a decentralized and open way. DeFi platforms allow users to lend, borrow, trade, earn interest, and even provide insurance, all without intermediaries.

Non-Fungible Tokens (NFTs)

Blockchain technology has also made a huge impact in the world of digital art and collectibles through Non-Fungible Tokens (NFTs). NFTs are unique digital assets verified using blockchain technology. They have provided a new way for artists and creators to sell their work and for collectors to prove their ownership of these digital assets.

Supply Chain, Healthcare, and More

The use of blockchain extends to many other industries:

- Supply Chain: Blockchain can provide transparency and traceability in supply chains, ensuring the authenticity of products, and tracking them from production to delivery.

- Healthcare: In healthcare, blockchain could secure patient data, manage drug supply chains, and enable transparent and efficient health service delivery.

- Voting: Blockchain can potentially solve issues related to voting fraud and low voter turnout by providing a secure, transparent, and easily accessible platform for casting votes.

- Real Estate: Blockchain can simplify the process of buying and selling property by reducing fraud, speeding up transactions, and providing transparency.

As more sectors begin to explore and implement blockchain, its transformative potential continues to grow. While challenges remain in terms of scalability and regulatory acceptance, the numerous applications of blockchain hint at a decentralized and transparent future.

Challenges and Criticisms of Blockchain

While blockchain offers many advantages, it's not without its challenges and criticisms. It's essential to be aware of these as we navigate towards a potential blockchain-dominated future.

Scalability

One of the main challenges facing blockchain technology is scalability. As the number of transactions increases, so does the size of the blockchain. This increase can lead to slower transaction times and higher costs, especially in public blockchains like Bitcoin and Ethereum. Various solutions have been proposed to address this, like sharding or layer 2 solutions, but these still are in their development or early adoption stages.

Environmental Concerns

Another significant criticism is the environmental impact of blockchains that use Proof of Work (PoW) consensus mechanisms. PoW involves solving complex mathematical problems which require a considerable amount of computational power and energy. Bitcoin mining is particularly notorious for its energy consumption, leading to criticisms about its sustainability.

Regulatory Issues

Finally, there are regulatory concerns surrounding blockchain technology. The decentralized, anonymous nature of public blockchains, particularly in cryptocurrencies, has raised concerns about their potential use for illegal activities. Additionally, there's a lack of clarity in many jurisdictions about how blockchain-based activities should be regulated and taxed.

In summary, while blockchain technology has vast potential, it's important to address these challenges to fully reap its benefits. As with any emerging technology, the journey of blockchain is bound to be filled with obstacles, but the progress made so far suggests a promising future.

The Future of Blockchain

With its disruptive potential, blockchain technology is set to play a crucial role in shaping the future, particularly in paving the way towards a more decentralized internet—Web3.

Role in Web3 and the Decentralized Internet

Blockchain's decentralized nature, combined with its transparency, security, and smart contract capabilities, aligns perfectly with the ideals of Web3. It forms the foundational layer for a new generation of decentralized applications (dApps) and services that put power back into the hands of users.

The future internet vision—Web3—sees users controlling their data and digital identities. Interactions on this internet version won't need intermediaries, thanks to blockchain-enabled trustless transactions. Smart contracts will automate agreement execution, further reducing reliance on third parties.

Emerging Trends and Advancements

As we move towards this future, several trends and advancements are emerging:

- Layer 2 solutions: Given the scalability challenges of current blockchains, layer 2 solutions like Ethereum's Optimism and Bitcoin's Lightning Network aim to process transactions off the main blockchain to increase speed and reduce costs.

- Interoperability: As the number of different blockchains grows, the ability for these systems to interact with each other becomes increasingly important. Interoperability could allow a user on one blockchain to seamlessly interact with a dApp on another blockchain.

- Proof of Stake (PoS): Given the environmental concerns associated with PoW, there's a trend towards using more energy-efficient consensus mechanisms like PoS. Ethereum's upcoming upgrade to Ethereum 2.0 is a prime example of this.

- Regulation: As blockchain continues to disrupt various industries, we can expect to see more regulatory frameworks developed. While these regulations may pose challenges, they can also provide a clearer environment for blockchain projects to operate within.

Blockchain technology is still relatively young, and it's evolving rapidly. The challenges it faces are significant, but the potential benefits it offers are even greater. If these challenges can be overcome, blockchain could be at the forefront of the next major technological revolution, driving the shift towards a decentralized, transparent, and user-centric internet—the Web3.

Conclusion

Blockchain technology has grown far beyond its initial application as the backbone of Bitcoin. Today, it is a revolutionary technology that promises to disrupt various industries and redefine how we interact on the internet. Its core features—transparency, immutability, security, and smart contract functionality—offer new ways to establish trust, streamline processes, and enable truly decentralized systems.

While blockchain faces challenges related to scalability, environmental impact, and regulatory acceptance, ongoing developments and increasing adoption are promising. As we move toward a decentralized internet—Web3—blockchain will undoubtedly play a pivotal role in shaping this future.